金融数据的交叉验证

传统验证方法在金融上为什么不行

像图像或表格数据,我们常用:

- K-fold cross-validation

- 随机划分训练/测试集

但是在金融(尤其是股市、币市)上:

价格数据是强时间相关的,而且分布随时间漂移(non-stationary)。

因此:

- ❌ 随机分割 → “未来数据”混进训练集(信息泄露)

- ❌ K-fold CV → 不符合时间因果

- ❌ 固定训练+测试划分 → 不能反映长期市场结构变化

这些都会让你的模型在训练集上表现很好,但实盘上全崩溃

在金融任务中,通常使用下列 3 种方法(越往下越贴近实盘)。

时间序列交叉验证 (TimeSeriesSplit)

优点:

- 简单易实现(

sklearn自带) - 不泄露未来信息

- 平衡“数据利用率”和“时序一致性”

使用场景:

- 模型结构、超参数调整阶段

- 适合验证模型的“平均泛化性能”

| 折数 | 训练数据 | 验证数据 |

|---|---|---|

| Fold1 | 1~100 | 101~150 |

| Fold2 | 1~150 | 151~200 |

| Fold3 | 1~200 | 201~250 |

滚动窗口验证 (Rolling Window Validation)

核心思想: 用固定长度窗口训练模型,然后滚动预测下一段时间。

优点:

- 模拟“定期 retrain 模型”的现实策略

- 反映模型对概念漂移 (Concept Drift) 的适应能力

示意图:

Train [1–100] → Predict [101–110]

Train [11–110] → Predict [111–120]

Train [21–120] → Predict [121–130]

特点:

- 窗口可以是固定长度(rolling)或扩展长度(expanding);

- 每次都重训模型;

- 非常适合高频交易或短周期预测。

Walk-Forward Validation (步进验证)

这是量化回测标准做法。

思路:

“在每个时点,只用已知历史训练模型,然后预测下一段时间。”

每次:

- 用过去数据训练;

- 预测未来;

- 滚动窗口前进;

- 累计所有预测,计算整体表现。

示意:

| 步 | 训练集 | 预测期 |

|---|---|---|

| 1 | 1–200 | 201–210 |

| 2 | 1–210 | 211–220 |

| 3 | 1–220 | 221–230 |

优点:

- 模拟真实交易中模型逐步更新;

- 无信息泄露;

- 适合回测策略;

- 可实时更新预测性能。

缺点:

- 计算量较大(每次都训练一个新模型);

- 实现稍复杂。

回测指标

仅仅看 MAE/MSE 不够。在金融中,更关心:

| 指标 | 含义 |

|---|---|

| Sharpe Ratio | 收益与风险比 |

| Max Drawdown | 最大回撤 |

| Hit Ratio / Accuracy | 方向预测正确率 |

| PnL(盈亏) | 模拟收益 |

| Calmar Ratio / Sortino | 回报稳定性 |

通常,我们会在 walk-forward 验证中:

- 模型预测未来一段收益方向;

- 构造简单交易策略;

- 回测计算上述指标;

- 得出真实金融表现。

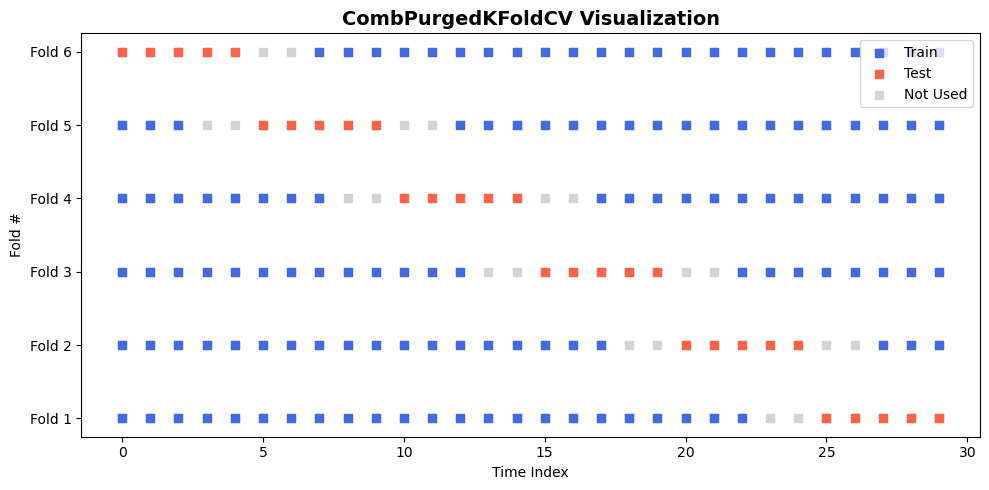

Purged & Embargoed Combinatorial Cross-Validation

这是 为金融时间序列设计的交叉验证方法, 专门用来:

- 防止 信息泄露 (Information Leakage),

- 防止 样本重叠 (Label Overlap),

- 在有时间依赖与事件窗口重叠的金融数据中,获得真实的泛化误差估计。

Purge(清除重叠样本)

- 删除所有训练样本中,

其

eval_time晚于测试集pred_time的样本。

这样训练集中不会包含与测试区间重叠的事件。

图示:

Train: |----A----|----B----|

Test: |----C----|

Purge: 删除B(因为B的eval_time> C的pred_time)

Embargo(时间缓冲区)

- 在测试集结束后,再空出一段时间, 不让太近的训练样本参与。

这段“冷却时间”叫 embargo period。

目的:

避免由于样本间时间相关性,训练数据太靠近测试数据而污染结果。

图示:

Train: |----A----| |----B----|

Test: |----C----|

<---embargo period--->

这样模型不会看到测试后太近的数据。

Combinatorial Cross-Validation

它的 “Combinatorial” 是因为:

它不是像普通 K-fold 那样一次一个 test fold, 而是从 n 个折中组合出若干个可能的测试集组合。

比如:

- 10 折(n_splits=10);

- 每次选 2 折当测试(n_test_splits=2);

- 所有 45 种组合都会测试一次。

这比单纯 10 次交叉验证要更全面, 能更稳定地估计模型的“泛化分布”。

预测时间和评估时间

在金融时间序列(比如比特币价格)里, 我们训练模型时,每一条样本其实对应一个“事件”:

- 在 预测时间 (

pred_time) 我们看到了特征,模型做出决策; - 在 评估时间 (

eval_time) 我们才知道这次决策到底对不对。

比如:

我在 10:00 预测比特币未来 5 分钟会上涨; 到 10:05 才能知道结果是否真的上涨。

所以每一条样本不是一个点,而是一段时间区间:

[ pred_time , eval_time ]

预测时间(pred_time)

t1 = pd.Series(t1_).shift(time_gap)

shift(time_gap) 的意思是“往后推 200 个单位”,

比如:

| 原始时间索引 | 预测时间 (t1) |

|---|---|

| 0 | 200 |

| 1 | 201 |

| 2 | 202 |

也就是说:

样本 0 对应的预测时间是 200(往后看 200 个单位)。

👉 模型在时间 200 才会用样本 0 的信息来预测。

评估时间(eval_time)

t2 = pd.Series(t1_).shift(-time_gap)

shift(-time_gap) 是往前推 200 个单位。

| 原始时间索引 | 评估时间 (t2) |

|---|---|

| 0 | -200 |

| 1 | -199 |

| 2 | -198 |

| … | … |

也就是说:

样本 0 的预测结果在 -200 的时候已经能验证。

换句话说:

- 在

pred_time时刻,我们知道输入特征。 - 在

eval_time时刻,我们才知道“真相”能否评估预测是否正确。

举例 👇

样本 A:pred_time = 10:00,eval_time = 10:05

样本 B:pred_time = 10:03,eval_time = 10:08

→ 每个样本代表一个「事件窗口」 [pred_time, eval_time]。

时间泄露(information leakage)

假设我们在训练模型时用了样本 A, 而在测试模型时用了样本 B。

那问题是:

样本 A 的评估结果(eval_time = 10:05) 其实落在了样本 B 的预测时间(pred_time = 10:03)之后!

这意味着:

- 当模型在测试时(10:03)进行预测,

- 它的训练样本(10:05 才结束)包含了未来的信息(10:05 > 10:03)。

这在金融里是致命的未来信息泄露 (look-ahead bias)。

purging 的作用

为防止这种泄露,purge 规则是:

任何训练样本,只要它的 评估时间 (eval_time) 晚于任何测试样本的 预测时间 (pred_time),就要删除。

形式化表达: $$ \text{如果 } eval_time(train) \ge pred_time(test) \Rightarrow 删除该 train 样本 $$ 这样可以保证:

- 训练样本用到的数据都比测试样本更早;

- 没有交叉时间窗口;

- 模型验证结果更接近真实交易情形。

from CombPurgedKFoldCV import CombPurgedKFoldCV

import numpy as np

import matplotlib.pyplot as plt

N = 30

cv = CombPurgedKFoldCV(n_splits=6, n_test_splits=1, embargo_td=1, look_after=2)

fig, ax = plt.subplots(figsize=(10, 5))

ax.set_title("CombPurgedKFoldCV Visualization", fontsize=14, weight="bold")

# 每一折绘制一行时间条

for fold_idx, (train_idx, test_idx) in enumerate(cv.split(np.arange(N))):

# 所有点背景置灰

ax.scatter(np.arange(N), np.ones(N)*fold_idx, color="lightgray", s=40, marker="s", label=None)

# 训练集蓝色

ax.scatter(train_idx, np.ones(len(train_idx))*fold_idx, color="royalblue", s=40, marker="s", label=None)

# 测试集红色

ax.scatter(test_idx, np.ones(len(test_idx))*fold_idx, color="tomato", s=40, marker="s", label=None)

# 图例 & 样式

ax.set_yticks(range(fold_idx+1))

ax.set_yticklabels([f"Fold {i+1}" for i in range(fold_idx+1)])

ax.set_xlabel("Time Index")

ax.set_ylabel("Fold #")

# 图例样例

ax.scatter([], [], color="royalblue", s=40, marker="s", label="Train")

ax.scatter([], [], color="tomato", s=40, marker="s", label="Test")

ax.scatter([], [], color="lightgray", s=40, marker="s", label="Not Used")

ax.legend(loc="upper right")

plt.tight_layout()

plt.show()

代码

顶层架构概览

整个代码有三层:

┌────────────────────────────────────────────┐

│ BaseTimeSeriesCrossValidator │ ← 抽象基类(模板)

├────────────────────────────────────────────┤

│ CombPurgedKFoldCV (子类实现) │ ← 具体交叉验证逻辑

├────────────────────────────────────────────┤

│ purge() + embargo() + 辅助函数工具层 │ ← 时间安全性控制工具函数

└────────────────────────────────────────────┘

思路:

- 上层定义“接口规范与统一检查”;

- 中层定义“交叉验证的分割策略”;

- 下层定义“时间安全机制(purge + embargo)”。

下面是 BaseTimeSeriesCrossValidator

from abc import abstractmethod # 定义一种不能直接实例化、必须被继承实现的类

import pandas as pd

class BaseTimeSeriesCrossValidator:

"""

抽象基类

为所有时间序列验证器提供统一接口和输入验证逻辑。

n_splits: 分成多少分, K-fold 的 K, >=2

"""

def __init__(self, n_splits:int=10):

self.n_splits = n_splits

self.pred_times = None

self.eval_times = None

self.indices = None

@abstractmethod

def split(self, X: pd.DataFrame, y: pd.Series = None,

pred_times: pd.Series = None, eval_times: pd.Series = None):

pass

下面是 CombPurgedKFoldCV

from BaseTimeSeriesCrossValidator import BaseTimeSeriesCrossValidator

import numpy as np

import itertools as itt

class CombPurgedKFoldCV(BaseTimeSeriesCrossValidator):

def __init__(self, n_splits = 10, n_test_splits=2, embargo_td=1, look_after=1):

super().__init__(n_splits)

self.n_test_splits = n_test_splits

self.embargo_td = embargo_td

self.look_after = look_after

def split(self, X, y = None):

self.indices = np.arange(X.shape[0])

# 按时间顺序切分数据成多个折

splited_indices = np.array_split(self.indices, self.n_splits)

all_bounds = [[block[0], block[-1]+1] for block in splited_indices]

# 枚举所有可能的测试组合

bounds_selection = reversed(list(itt.combinations(all_bounds, self.n_test_splits)))

for bounds in bounds_selection:

test_indices, test_bounds = self.compute_test_set(bounds)

train_indices = self.compute_train_set(test_indices, test_bounds)

yield train_indices, test_indices

def compute_test_set(self, bounds):

# 如果相邻的测试折是连续的,就把它们合并成一个区间

merged_bounds = []

for x in bounds:

if not merged_bounds or merged_bounds[-1][1] != x[0]:

merged_bounds.append(x)

else:

merged_bounds[-1][1] = x[1]

test_indices = np.array([], dtype=int)

for l,r in merged_bounds:

test_indices = np.concatenate((test_indices, self.indices[l:r]))

return test_indices, merged_bounds

def compute_train_set(self, test_indices, test_folds):

train_indices = np.setdiff1d(self.indices, test_indices)

for test_fold in test_folds:

train_indices = self.purge(train_indices, test_fold[0])

train_indices = self.embargo(train_indices, test_fold[1])

return train_indices

def purge(self, train_indices, test_fold_start):

# 保证 train 的 eval_time < test 的 pred_time

overlap = [i for i in train_indices if (i + self.look_after) >= test_fold_start and i < test_fold_start]

train_indices = np.setdiff1d(train_indices, overlap)

return train_indices

def embargo(self, train_indices, test_fold_end):

# test end 后一段时间不允许出现 train sample

overlap = [i for i in train_indices if test_fold_end <= i <= test_fold_end + self.embargo_td]

train_indices = np.setdiff1d(train_indices, overlap)

return train_indices